The European Union

During the Cold War European capitalists attempted to form a bloc to defend themselves, on the one hand, against the might of the USSR, on the other hand, against the encroaching power of the USA. The collapse of the USSR and the achievement of a unified Germany in 1989 gave a further impetus to European economic integration. The German bourgeoisie and its political representative Kohl, had big ambitions. The euro was in large part an attempt by Berlin to achieve by economic means what Hitler attempted to do by force – to unify Europe under German domination.

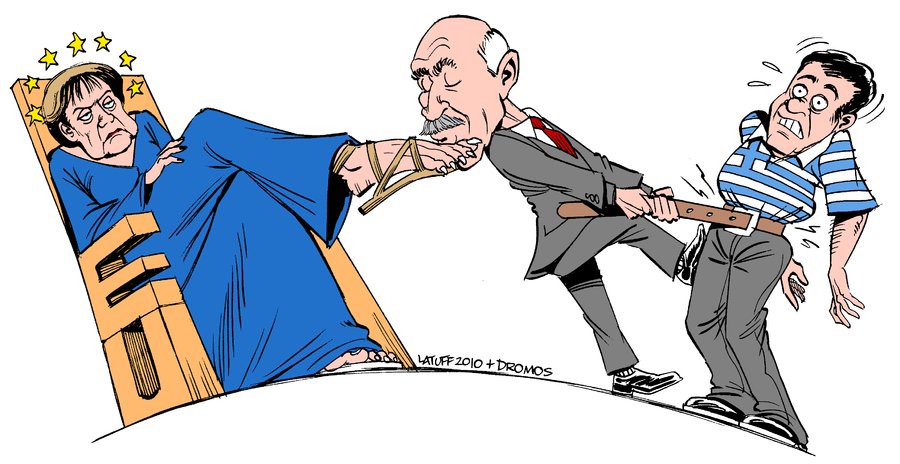

Drawing by LatuffThe

euro zone has a single central bank, the European Central Bank (ECB),

and therefore has only one monetary policy, regardless of whether it is

located in Athens or Berlin. But in reality, the whole project was

dominated by German capital. Initially, Germany benefited from free

access to other European markets, and the others benefited from access

to seemingly unlimited supplies of capital, investment, loans, grants

and credits. Everything seemed to be for the best in the best of all

capitalist worlds.

Drawing by LatuffThe

euro zone has a single central bank, the European Central Bank (ECB),

and therefore has only one monetary policy, regardless of whether it is

located in Athens or Berlin. But in reality, the whole project was

dominated by German capital. Initially, Germany benefited from free

access to other European markets, and the others benefited from access

to seemingly unlimited supplies of capital, investment, loans, grants

and credits. Everything seemed to be for the best in the best of all

capitalist worlds.

In order to convince Berlin to share its currency with the rest of Europe, it was agreed that the euro zone should be modeled after the Bundesbank. The Euro itself was to be as strong as the deutschmark. As a condition for joining the euro zone, every country had to agree to rigorous “convergence criteria”. These were intended to synchronize the economy of the member states with that of Germany.

These criteria included a budget deficit of less than 3 percent of gross domestic product. Government debt levels were to be no more than 60 percent of GDP. An annual inflation could be no higher than 1.5 percentage points above the average of the lowest three members’ annual inflation. Now all these plans lie in ruins. As we predicted more than ten years ago, it is impossible to achieve convergence criteria for economies that are moving in different directions. Greece’s failure to comply with the Growth and Stability Pact is only the most blatant case. But the truth is that from the very beginning none of the euro zone member states — including France and Germany — have complied with the rules.

Now deep cracks have opened up which threaten to bring down the whole artificial construction and bury all the dreams of a united capitalist Europe. Sarkozy at one point threatened to pull out of the single currency if Germany didn't agree to pay up.

Big banks in France and Germany would be devastated if there was default in Greece or Portugal, since they have lent most of the money.

Will the euro zone break up?

The trouble with the euro is that it attempts to unite economies that are pulling in different directions. The European bourgeois are striving with all their might to keep the currency union together. They are acting on the old thieves’ saying: either we hang together or we will hang separately. But the crisis has revealed the underlying fault lines that threaten to break the euro zone apart and even pose a question mark over the future of the European Union itself. The tensions are increasing all the time.

When the euro was born a decade ago, it came with central rules limiting budget deficits and banning bail-outs. Yet the rules, which theoretically included huge fines for excessive borrowing, were never likely to stick, and were soon emasculated by France and Germany. The financial markets assumed that no euro-area country would ever be allowed to go bust: they assumed that the European Central Bank would always come to the rescue. Now, despite the latest bailout, this can no longer be taken for granted.

This time, Germany has agreed to back a “rescue fund”. But there are profound tensions in Germany. If the crisis deepens and the national tensions increase, it could possibly cause Germany to quit the euro zone altogether. The idea is rapidly gathering ground in Germany that Greece and the euro zone’s other weaker economies should be excluded from the currency union if they do not pay their debts. At one point it seemed that Chancellor Merkel herself was in favour of this.

It is therefore not at all ruled out that the present crisis will end with the “reconstitution” of the Euro zone, either by the expulsion of Greece or the withdrawal of Germany. But the latter variant would mean in effect, the total breakup of the experiment. It would plunge world currency markets into a deep crisis and wreck the weak economic revival.

If Greece were to withdraw from the euro, its central bank could print money and purchase government debt, bypassing the credit markets. It would also allow Athens to devalue, which would stimulate external demand for Greek exports and spur economic growth. The alternative is to resort to a painful “internal devaluation” via austerity measures demanded by the International Monetary Fund (IMF) and the EU.

The problem is that no one would want this new currency, particularly because it would be clear to everyone that the government would only be reintroducing it to devalue it. In effect, the drachma would only be accepted within Greece, and even there it would not be accepted everywhere. It would lead immediately to a black market, which would have to be put down by force. The cost of exit would therefore be prohibitively high.

How can the present crisis be resolved? In theory, the expulsion of member states is illegal. In any case, it would have to be approved by of all 27 member states, which poses the intriguing question: why should Greece approve its own expulsion? Even if it could be arranged, it is clear that Portugal, Spain and Ireland would not be very keen to vote for a measure that would provide a precedent for their own exclusion in the not-too-distant future.

Of course, there are very clever people sitting in Brussels whose creative powers can surely enable them to think of some bureaucratic solution that would bend the rules to allow the European Union to get rid of undesirable members without formally breaking the treaties. They could, for instance, set up a new European Union with a new “strong” euro zone, minus Greece (and any other awkward customers).

Such a step would eliminate one problem, but only at the cost of creating many new contradictions. Germany would greatly increase its power, and that is not something the rest of Europe would be enthusiastic about. In a new euro zone composed of, say, France and the Benelux countries, Germany’s economy would represent 45.6 percent of overall output, as opposed to 26.8 percent of euro zone now. Moreover, the excluded states might take their revenge by defaulting on their debts, which would have a devastating effect on the new euro zone.

Parasitism of capitalists

The bourgeois has long ago lost all interest in productive activity and productive investment. It seeks to make money out of money without having to bother with the painful and risky process of production. With a few exceptions, like China, where huge profits can be made from the exploitation of a vast pool of labour from the countryside, the bourgeoisie has tended to rely more and more on the parasitic service sector, and especially the financial sector. That is why they always present the crisis as a crisis of credit.

This is an entirely mystical way of presenting the question. Credit can never play an independent role in the economy. Credit is only a way of expanding consumption beyond its natural limits, either individual consumption of commodities, or the consumption of machinery, raw materials and labour power by the capitalists themselves.

The purely parasitic nature of modern capitalism is seen by the fact that when the banks ran up huge debts, the state immediately stepped in to shower them with vast amounts of public money. The bankers said “thank you very much” and then proceeded to pocket the money, or pour it into a black hole (nobody knows how deep it is or where it leads), helping themselves to generous bonuses in the process.

There is no sign of all this massive injection of public funds into the banks having any serious effect on the real economy. Economic life remains at a very low level and unemployment remains stubbornly high. There is very little real gain to be shown for such a huge expenditure of public money. The reason is not hard to explain. Given the huge amount of excess capacity on a world scale, there is little or no incentive for the capitalists to spend large sums of money on productive investment. There is one third excess capacity in the car industry on a world scale. Why should Ford and General Motors build new plants, when they already have too many factories and not enough paying customers?

“The banks must be saved!” That is all. The politicians immediately come running with an open cheque book. And the Social Democrat politicians run faster than anybody else. Having “saved the banks” (that is, having saved the bankers), the politicians then sadly inform a bewildered public that, well, actually, we never had the money to pay the bankers in the first place. We had to borrow it in your name and now you must pay it all back. Time for sacrifice!

Once the banks have pocketed the money of the state, the markets (that is to say, the same bankers) suddenly begin to shout: “Look! There is an unsustainable level of public debt! This must be paid immediately!” In the midst of this unholy hullabaloo, nobody asks the simple question: Why is there a high level of public debt? And nobody asks where all the money has gone to. Here we enter the mysterious realm of banking secrets, which must be maintained as absolutely as the secrets of the confession box in church.

What is the “credit crunch”?

As long as the world capitalist economy was going forward, markets were booming, profits were soaring, credit was easy. Nobody looked too closely at the balance sheets of companies, banks or nations. Everybody was enjoying the merry carnival of money making. The values on the stock exchange are soaring to heights that bear no relation to the real economy? Let them soar! The banks are lending money they do not have? Let them lend! Greece wants to borrow a billion or two? Let them have it!

But when the day of reckoning comes (as it always does) the mood of the bourgeois changes abruptly. Now nobody wants to lend money. On the contrary, they are all calling in their debts. Instead of the former cheerful open-handedness, there is a mean and grasping mentality, like that of a miser who greedily hoards his loot and guards it jealously so that nobody will see how much he has got. Hoarding is a typical feature of primitive capitalism in its early stages. In a crisis, it is as if the bourgeois have returned to their beginnings, like a man in the stage of decrepit senility who returns to a second childhood.

Now nobody wants promissory notes. They do not want promises of any kind, because they no longer trust anybody: creditors, bankers or governments. They want the real thing. They want cash in hand. And they want it now. This meanness takes no account of the real problems faced by families, businesses or governments. You do not have enough food to eat? Then starve, but pay me what you owe. Your business will have to close, and hundreds will lose their employment? Then close it, and be damned, but pay up! And if this absolute rule of Capital is appropriate in the case of individuals and businesses, why should a nation state be any different? It is the business of Capital to make money. Whatever problems may arise from this money-making activity is an irrelevant matter.

Marx describes this tendency to hoard money in a crisis:

“Countries in which the bourgeois form of production is developed to a certain extent, limit the hoards concentrated in the strong rooms of the banks to the minimum required for the proper performance of their peculiar functions. Whenever these hoards are strikingly above their average level, it is, with some exceptions, an indication of stagnation in the circulation of commodities, of an interruption in the even flow of their metamorphoses.” (Capital, vol. 1, Section 3, Money, c) Universal Money)

The role of gold

Paper money is only a promise to pay. In the past it was backed by gold and silver. But in the age of the senile decay of capitalism the bourgeois imagined that it could do without gold altogether. The bourgeois economists talked of the “demonetization of gold”. This is complete nonsense. Gold is a commodity, and like all other commodities, has an objective value, determined by the amount of socially necessary labour power expended on its production. Its value as a commodity is high because it is relatively rare and there are high costs involved in its discovery and exploitation.

However, gold has historically evolved as “the commodity of commodities” – that commodity through which all other commodities express their values, that is, money. It is a standard of price, and also serves as a universal measure of value, the equivalent commodity par excellence, to use Marx’s expression.

The Bretton Woods agreement of 1944, which set up the international monetary regime that prevailed from the end of World War II until the early 1970s, established the dollar as the medium of world trade (with the pound sterling as a secondary currency). In reality, however, currencies were still pegged to gold at a value fixed in dollar terms.

At that time the USA could dictate terms to the rest of the world. After the War, the productive apparatus of the USA was intact, while Europe and Japan were devastated. Two thirds of all the gold stocks in the world were in Fort Knox. The dollar was therefore “as good as gold”.

When the United States abandoned the gold standard in 1971, Washington liquidated the Bretton Woods agreement that pegged currency to gold. Currencies were allowed to float. While the U.S. dollar was still regarded as the world currency, the deutschmark began to emerge as a strong contender for this role.

The paper currencies in use throughout the world today are no longer backed by gold. Therefore they hold no value except the political decision to make them the legal tender of commercial activity. Refusal to accept paper currency is, within limitations, punishable by law. But this means governments must be willing and able to enforce the currency as a legal form of debt settlement. But what happens if a government has such a high level of debt that it is unable to meet its liabilities?

By abandoning the link to gold, the bourgeoisie created the conditions for the kind of currency competition and beggar-my-neighbour devaluations that was one of the main factors that transformed the crisis of 1929 into the Great Depression of the 1930s. In the last few years the US authorities were content to see the dollar slide against the euro and other currencies in order to boost its exports to the rest of the world.

Some of the more obtuse politicians actually believed the nonsense of the bourgeois economists about the “demonetization of gold”. Thus, Gordon Brown sold off Britain’s substantial gold reserves between 1999 and 2002, and in the process obtained a mere $4bn for what today would be worth more than $15bn. This little detail reveals at once the intellectual bankruptcy of bourgeois political economists and reformist politicians, which, in this case, contributed directly to national bankruptcy.

The flight into gold

As the credit ratings of Greece, Spain and Portugal fall, so the world market price of gold is soaring far more than most other commodities. This always happens in a crisis, when the capitalists look for a safe harbour to shelter from the storm. In uncertain times, the financial gamblers of yesterday suddenly lose their taste for risky operations. The hard-headed men of money are no longer interested in paper money, or promises of any sort, whether from private individuals, bankers or Greek Prime Ministers. They want only the real thing: cash in hand, ready money – real money, that is, gold.

Let the academics, the professors of economics with long lists of letters after their name, deliver lectures on the demonetization of gold. Those who really hold our economic destinies in the palm of their hand, are unimpressed by such lectures, which only confirm them in their instinctive belief that the most ignorant people in society are to be found between the four walls of universities. Instead, they repeat the words of Shakespeare in Timon of Athens:

“Gold? Yellow, glittering, precious gold?

No, Gods, I am no idle votarist! ...

Thus much of this will make black white, foul fair,

Wrong right, base noble, old young, coward valiant.

... Why, this

Will lug your priests and servants from your sides,

Pluck stout men’s pillows from below their heads:

This yellow slave

Will knit and break religions, bless the accursed;

Make the hoar leprosy adored, place thieves

And give them title, knee and approbation

With senators on the bench: This is it

That makes the wappen’d widow wed again;

She, whom the spital-house and ulcerous sores

Would cast the gorge at, this embalms and spices

To the April day again. Come, damned earth,

Thou common whore of mankind, that put’st odds

Among the rout of nations.”

The bourgeois are anxious to get their hands on gold, hoping its glitter will defy the laws of economics and maintain their fortunes until the dawn of better times. Indeed. Long before the crisis of 2007 many financial speculators were already getting rid of paper money and building up their stock of bullion. As soon as that happened, savvy shoppers followed. The big-time investors, as always, led the way, and are now being followed by everyone else, pushing the price of gold to astronomic levels.

Refineries in South Africa say they are overwhelmed by orders from Germany for Krugerrand gold coins. This indicates that ordinary people are buying gold, not just professional investors. In Germany memories of hyper-inflation in the 1930s still survive. The Austrian mint says it ran out of its stock of similar coins last week, as the price of an ounce of gold passed through the €1,000 barrier for the first time.

The “speculators” (read, capitalists) do not have any faith in the euro, and still less in the pound sterling. The dollar has risen recently, but this is a sign of desperation and the weakness of alternative currencies. It is certainly not justified by the strength of the US economy or the state of its finances. Under these conditions one would expect to see a flight from paper money into gold and other things that may hold or increase their value (works of art). And that is just what we are seeing.

Germany

The European bourgeois are looking to the future with dread. They must tread carefully, because they are walking on a minefield. With every step they take, the bourgeoisie and its political representatives must constantly look over their shoulders to see how the working class is reacting. That is the main problem. After decades of relative prosperity, the working class will not allow their living standards to be destroyed without a fight. And that is just as true of the German workers as it is in Greece.

Merkel paid the price on May 9th, when she suffered her worst political defeat in more than five years in office. The very evening when European finance ministers were meeting in Brussels to defend the stability of the euro, voters in North Rhine-Westphalia (NRW), Germany’s most populous state, ejected the chancellor’s allies from office. Voters unseated a coalition between her Christian Democratic Union (CDU) and the liberal Free Democratic Party (FDP) similar to the one in Berlin.

Merkel was not to blame for the euro crisis but when it came she delayed taking measures. On the one hand she wanted to exert extra pressure on Greece, but also Spain, Italy and Portugal to introduce draconian austerity packages. On the other she was hoping that bail-outs of Greece and other weak euro-zone members could be put off until after NRW’s election. But the delay only made matters worse. The defeat in NRW has deprived the Merkel government of its majority in the Bundesrat, the upper house of the legislature, which represents the states. To enact most money bills the government will now have to co-operate with the opposition.

The economic crisis is causing divisions at the top that sooner or later must lead to an open split in the government. The pressure will mount. Everyone is in favour of deficit reduction in principle but in practice it is another matter. Merkel now presents herself as the guardian of economic stability. But who will decide where the axe will fall? Some suggest cuts to education and child care. Health-care is another candidate for “reform” – that is, the axe. The crisis of the bourgeoisie is shown in the contradictory advice given to Merkel: “Be bold”, she is told, “but do not offend the voters”. How this miracle is to be accomplished we are not informed.

The bourgeoisie faces a dilemma, not just in Germany but in all Europe. The seriousness of the economic crisis means that they will have to inflict deep cuts on the workers and the middle class, but the social and political consequences of such actions will completely undermine them. To solve this dilemma is only slightly more difficult than trying to square the circle. Every attempt to restore the economic equilibrium will destroy the social and political equilibrium.

The German bourgeoisie is resentful of bail-outs, fearful about the euro’s stability and increasingly unwilling to identify Germany’s interests with those of Europe. This is a far cry from the grandiloquent speeches of Kohl about European unity and Germany’s role at the centre of it.

World economy

The looming crisis looks very similar to the last, with the financial system, and banks in particular, at the centre. This fact reflects the fundamental sickness of capitalism in the epoch of its senile decay. What now being presented as a monetary crisis will become a prolonged economic and political crisis affecting every country in Europe.

The U.S. capitalists were hoping that they could dramatically increase exports to Europe. But the steep drop in the value of the euro (about $1.25, down from more than $1.50 in November 2009) makes American goods more expensive compared with those produced in Europe. The American economy will be hard hit by a new banking crisis and a fall in exports to Europe. It would be harder to borrow money or raise finance for businesses.

In a crisis the banks stop lending to each other and begin closing down credit lines, sparking a chain reaction throughout the financial system. The banking systems in Europe and the United States are closely interconnected and European banks must have serious repercussions in the USA.

Daniel Tarullo, a member of the Federal Reserve's board, recently warned that a repeat of the 2008 crisis which saw the near collapse of the US financial sector was "not out of the question." He told Congress last week that banks were going through spasms that "brought back memories of developments during the recent global financial crisis." The decline in the common European currency also makers it less likely that China will accept with U.S. demands to raise the value of their money, making it easier for U.S. products to compete.

To be continued